Tax Rate Reduction Implication to Fiscal Year Companies

IRS Notice 2018-38

Internal Revenue Code (IRC) section 11(b) provides that the rate of corporate income tax is 21% effective for tax years beginning after December 31, 2017. Additionally, the alternative minimum tax (AMT) tax imposed under IRC section 55 has been repealed effective for tax years beginning after December 31, 2017. For a fiscal year end corporation’s taxable year beginning before January 1, 2018 and ending after December 31, 2017 (the “transition period”), under IRC section 15, the effective date of these tax law changes is as of January 1, 2018. In other words, tax liability of a fiscal year end corporation must be computed using both old and new tax law for the transition period.

The IRS issued Notice 2018-38 (the “Notice”) providing guidance how tax liability should be computed during the transition period for a fiscal year end corporation. Under the guidance, a corporation with a fiscal year that includes January 1, 2018, computes federal income tax using a blended tax rate approach and the following example illustrates how the rule applies.

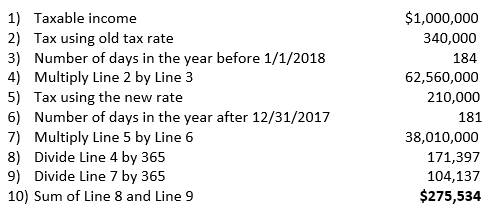

Example I – IRC sections 11(b) & 15(a)

Corporation X reports $1,000,000 of taxable income for its fiscal year ending June 30, 2018. Corporation X’s federal tax liability is $275,534, as computed below.

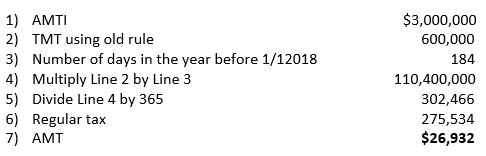

Example II – IRC sections 55 & 15(a)

Corporation X reports $1,000,000 of taxable income and $3,000,000 AMTI for its fiscal year ending June 30, 2018. Corporation X’s AMT tax liability is $26,932, as computed below.

Please refer to the Notice 2018-38 https://www.irs.gov/pub/irs-drop/n-18-38.pdf for additional detail.